UK Gambling Tax Rise Explained

The UK gambling tax rise may raise Treasury revenue, but 40 percent Remote Gaming Duty could weaken licensed operators, reduce competition and push some players towards black market gambling sites.

Reviewed by Stephen Tabone for Global Casino Games. Last reviewed: 05 June 2026.

Why 40 Percent Remote Gaming Duty Could Backfire

The UK gambling tax rise may raise Treasury revenue, but 40 percent Remote Gaming Duty could weaken licensed operators, reduce competition and push some players towards black market gambling sites.

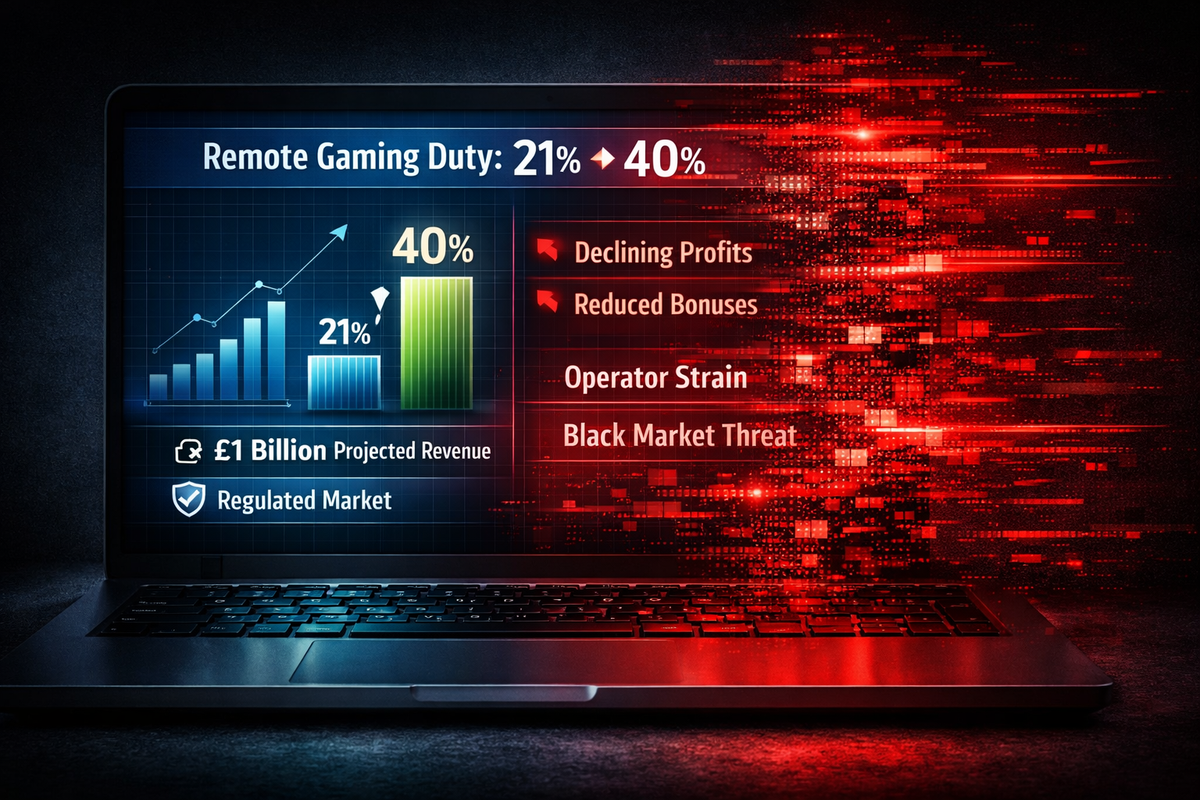

The UK has raised Remote Gaming Duty from 21 percent to 40 percent, placing online casino games and slots under heavy tax pressure. The government says the rise targets higher-risk products, supports public finances and modernises gambling taxation. Global Casino Games argues that the rate went too far, too quickly, and should be reduced before it damages the regulated market.

Source data in this article reflects public information available at the time of writing in June 2026.

UK Gambling Tax Rise At A Glance

| Gambling Product | Previous Rate | New Rate & Effective Date |

|---|---|---|

| Online casino games and slots | 21% | 40% (From April 2026) |

| Remote sports betting | 15% | 25% (From April 2027) |

| Remote betting on UK horse racing | 15% | Stays at 15% |

| Self-service betting terminals (Licensed premises) | 15% | Stays at 15% |

| Bingo Duty | 10% | Abolished (From April 2026) |

HMRC confirms that Remote Gaming Duty rose from 21 percent to 40 percent from 1 April 2026. HMRC also confirms the new 25 percent remote betting rate from April 2027, while UK horse racing and self-service betting terminals in licensed premises remain at 15 percent. Bingo Duty has been abolished from April 2026.

The table shows the policy direction clearly. The government did not apply one flat tax across gambling. It aimed the largest increase at online casino games and slots.

What Changed In UK Gambling Tax From April 2026?

The UK gambling tax rise is not a minor adjustment. It changes the economics of online casino gaming, operator margins, betting shops, advertising, affiliate revenue and player value.

HMRC says the package should raise more than £1 billion per year for the public finances. Its published impact table estimates £810 million in 2026 to 2027, rising to £1.155 billion by 2030 to 2031.

The official logic is straightforward. Online casino games and slots are seen as lower-cost remote products with higher harm risk. HMRC says the Remote Gaming Duty rise aims to discourage operators from pushing consumers towards those products.

That is a serious policy aim. Gambling harm is real, and any responsible iGaming publication should acknowledge it.

The problem sits in the design. A sharp rise from 21 percent to 40 percent almost doubles the rate. That kind of shock can reshape the licensed market before policymakers fully measure the consequences.

Why The UK Gambling Tax Rise Could Reshape Online Casino Gaming

Imagine two players looking for a casino offer.

One player uses a UK-licensed casino. The site checks identity, follows safer gambling rules, applies technical standards and offers a modest promotion.

Another player finds an offshore site offering a huge bonus, fewer checks and instant access. The offer looks bigger. The protection sits on weaker ground.

This is the real issue behind the UK gambling tax rise. It is not only a Treasury measure. It is a pressure test for the regulated market.

When tax rises sharply, operators review margins, promotions, advertising, affiliate deals, staffing, betting shops and investment. The cost does not stay trapped inside a spreadsheet.

The ripple effect is easy to follow. Higher tax squeezes operator economics. Squeezed operators reduce player value. Weaker value gives illegal gambling sites a cleaner opening.

That is where the policy becomes fragile.

Why Did The Government Raise Remote Gaming Duty?

The government’s argument has three main parts.

First, online casino games and slots are viewed as higher-risk products. Second, remote gaming has grown quickly. Third, the Treasury wants more revenue from a sector it sees as profitable and lower-cost to operate.

HMRC says remote gaming generally has lower operating costs and is considered more harmful than other forms of gambling. The stated aim is to disincentivise companies from pushing consumers towards those products.

HMRC also accepts that the duty rise could reach players through worse odds or lower return to player. Its own impact note says some individuals could switch to other gambling activities or use the illegal gambling market.

That admission is crucial. The government’s own assessment recognises a risk of player movement.

So the debate is not whether online casino gambling carries harm. It does. The harder question is whether 40 percent Remote Gaming Duty protects the regulated market or weakens it.

The scale of this fiscal and enforcement battleground can be seen clearly when looking at the official projections against active tracking data:

The Fiscal vs. Enforcement Battleground

Comparing the Treasury's projected tax gains against the massive scale of active black market suppression.

Projected Annual Tax Revenue

Regulator Takedowns (Since April 2024)

Is Remote Gaming Duty A Tax On Deposits Or Gambling Profit?

Remote Gaming Duty is not best described as a tax on every customer deposit.

HMRC applies Remote Gaming Duty to remote gaming profit from UK customer activity. The Office for Budget Responsibility also describes Remote Gaming Duty as a tax on gaming provider profits and notes the increase from 21 percent to 40 percent from April 2026.

In plain English, the tax follows the UK-facing gambling profit. It does not simply attach to every pound a player deposits.

This distinction explains the pressure on licensed operators. If UK customer play creates remote gaming profit, UK gambling duty can apply.

The cost then has to land somewhere. Operators can accept lower margins, reduce promotions, tighten loyalty offers, cut marketing, reduce affiliate spend or slow investment.

None of those responses automatically improves player protection.

Can UK Online Casinos Avoid Remote Gaming Duty By Moving Offshore?

Licensed operators cannot simply move abroad and escape the UK duty.

The Office for Budget Responsibility explains that UK gambling duties work on a place of consumption basis. Remote gambling operators pay UK gambling duty on gross gambling profits from UK customers, regardless of where the operators are located.

In practical terms, the tax follows UK customer activity. If a player in London, Manchester, Cardiff or Glasgow plays through a UK-facing licensed remote casino, the duty can still apply to the operator’s UK customer profit.

Malta, Gibraltar, the Isle of Man, Ireland or another base does not remove the UK duty from British customer play.

Readers should separate lawful offshore corporate structures from illegal offshore gambling. A licensed operator can sit outside the UK and still follow British licensing, tax and compliance rules.

An illegal operator targets UK players without that same framework.

For licensed firms, the duty follows UK customer activity. The black market faces no equivalent pressure.

Why 40 Percent Remote Gaming Duty May Be Too High

Gambling should be taxed. The serious objection is the size and speed of this rise.

A move from 21 percent to 40 percent represents a near doubling of Remote Gaming Duty. A more measured increase towards 25 to 30 percent would still have raised the burden. It would also have given the licensed market more room to absorb the change.

Global Casino Games’ view is clear. The rate went too far, too quickly.

Large operators can rely on scale. They can spread compliance, technology, product and marketing costs across several brands and countries.

Smaller operators face a harsher equation. The pressure usually lands in promotions, loyalty rewards, affiliate deals, staffing and product investment.

Some brands will absorb the hit for a period. Others will merge, sell, reduce their UK ambition or leave weaker parts of the market.

For players, the tax will not arrive as a visible bill. It will appear through worse value, tighter offers and a less competitive licensed market.

How Does UK Online Casino Tax Compare With Europe?

European comparison does not produce one neat league table. Some countries tax gross gaming revenue. Others tax stakes, public levies, advertising or product-specific activity.

The useful question is different. Does the tax structure keep players inside the regulated market?

The UK now taxes online casino gaming at 40 percent through Remote Gaming Duty. Spain generally applies 20 percent of gross gaming revenue to licensed online gambling, with a reduced 10 percent rate for operators based in Ceuta or Melilla. Italy applies a GGR-based regime where online products sit around 24.5 to 25.5 percent, depending on the product.

That does not make Spain or Italy weak regulatory markets. Both treat gambling seriously. Their online casino tax rates simply sit far below the UK’s new 40 percent rate.

A lower regulated tax burden gives legal operators more room to compete on bonuses, loyalty, product quality and marketing. A higher burden squeezes that space.

The UK has not only raised tax. It has made licensed online casino gaming harder to price competitively against illegal alternatives.

Spain And Italy Show Lower Online Casino Tax Pressure

Spain and Italy offer useful comparisons because both operate regulated online gambling markets inside Europe.

Spain’s general online gambling tax sits far below the UK’s 40 percent Remote Gaming Duty. Italy’s online casino rate, even after recent adjustments, sits around 25.5 percent of gross gaming revenue.

This difference affects consumer value. A legal operator taxed at 20 or 25.5 percent has more room to fund promotions, media spend, product improvement and retention offers than one taxed at 40 percent.

That does not prove lower tax always works better. It does show how aggressive the UK position has become.

Germany Shows How Bad Gambling Tax Design Can Hurt Player Value

Germany shows a different warning.

Germany applies a 5.3 percent tax on stakes for sports betting, horse racing, virtual slots and online poker. That looks lower than the UK’s 40 percent Remote Gaming Duty, but stake taxes bite before final gambling profit is known.

ICLG notes that Germany’s stake tax is particularly high for virtual slot games. It also notes that the tax caused a dramatic drop in return to player and has faced legal challenge.

Germany therefore supports a wider point. Bad tax design can damage player value even when the headline number looks lower.

A legal market can exist on paper while becoming less attractive in practice.

France Shows The Side Effects Of Heavy Gambling Levies

France is not a clean online casino comparison because online casino games remain prohibited. French online gambling focuses on licensed sports betting, horse racing and poker.

Even so, France shows how heavy levies can affect operator economics.

FDJ United reported that online sports betting public levies rose from 54.9 percent to 59.3 percent of gross gaming revenue. It also reported that online poker moved from 0.2 percent of stakes to 10 percent of gross gaming revenue.

France also introduced a 15 percent tax on betting and gaming advertising and promotional expenses from July 2025, excluding horse racing. FDJ United reported that the French advertising and promotion tax would affect operator costs from 2025 into 2026.

The European pattern is clear. Governments are using gambling tax more aggressively.

The risk is just as clear. If regulated operators carry too much fiscal weight, the legal market can lose the flexibility needed to compete.

Could Higher Gambling Tax Reduce Competition In The UK Casino Market?

Competition is one of the most important parts of this debate.

A healthy regulated market needs real pressure between operators. That pressure keeps service, value, product quality and customer experience alive.

The UK market already contains major gambling groups with several brands. The Competition and Markets Authority cleared the Flutter and Stars merger in 2020. At the time, the CMA said Flutter owned Paddy Power and Betfair, while Stars owned Sky Bet, and that the businesses had combined UK revenue of about £1.5 billion.

Consolidation does not always harm players. Larger groups can invest in safer gambling systems, security, technology and compliance.

Too much concentration creates a different problem. If fewer groups own more brands, players see fewer genuine alternatives. Promotions tighten, loyalty offers weaken and customer service pressure can fall.

Competition keeps markets honest. If an operator knows players can move easily, it has a reason to improve.

If high tax removes smaller challengers, the regulated market may remain legal but become less competitive.

Will Gambling Tax Consolidation Hurt Player Choice?

The danger is not only that some operators struggle. The deeper risk is that the market narrows around a smaller group of dominant firms.

Large groups can absorb 40 percent Remote Gaming Duty through scale, shared technology and international revenue. Smaller brands operate with less protection.

When smaller firms sell, merge or leave, the casual player can lose choice without noticing the cause. The website names may remain, but ownership and pricing power may sit inside fewer corporate structures.

That can weaken player value over time.

A market with more genuine competitors pushes operators to improve offers, payout speed, product design, customer support and loyalty schemes.

A market with fewer real challengers has less pressure to stay generous.

Does Foreign Ownership Make UK Gambling Regulation More Complex?

Foreign ownership is not automatically bad. Many international operators run compliant UK-facing businesses.

A UK licence remains central. UK gambling rules continue to apply. UK tax obligations do not vanish because ownership sits abroad.

The issue is strategic complexity.

When major UK-facing brands sit inside global groups, key commercial decisions may sit outside Britain. A global operator can compare the UK with markets that offer lower tax, faster growth or lighter commercial pressure.

That does not mean a foreign owner will abandon the UK. It means the UK must compete for investment inside global capital structures.

A group may keep a UK licence but shift product ambition elsewhere. It could lower marketing spend, slow innovation or focus growth capital on other jurisdictions.

The UK would still have a regulated market. It could become less energetic, less diverse and less responsive to players.

Why Black Market Gambling Is The Main Risk

The black market is not a slogan. It is an active enforcement problem.

The Gambling Commission says illegal operators undermine consumer protection, create unfair competition and do not contribute tax, levies or funding for sport. It also says illegal operators can threaten sporting integrity and link to wider criminality.

The regulator’s own data shows the scale of enforcement.

Since April 2024, the Gambling Commission’s Illegal Markets team issued 3,140 cease-and-desist or disruption notices. It referred 447,778 Bing and Google URLs and had 287,961 URLs removed.

Those figures tell two stories at once. The regulator is active. The illegal market also keeps regenerating.

Tax policy cannot ignore that enforcement reality. If licensed sites become less attractive, illegal operators do not need to become safe.

They only need to look tempting.

The Economic Equilibrium. Keeps the vast majority of consumers inside licensed safe zones while optimizing government yield.

Player Channelisation Rate

Percentage of active domestic consumers staying entirely within UK identification and harm prevention nets.

Offshore Black Market Leakage

Estimated annual volume of consumer wagering turnover completely evading UK taxation and operator audits.

Could The Treasury Win Short Term And Lose Long Term?

In the short term, the government may raise more revenue. Official forecasts say it will.

The longer-term risk sits elsewhere.

If licensed operators cut investment, reduce marketing, lower affiliate spend, close betting shops, merge or shift growth capital abroad, the regulated ecosystem becomes thinner.

If some players move to illegal sites, the Treasury collects no duty from that activity.

The regulator also loses visibility. Safer gambling tools weaken. Disputes become harder to resolve. Game fairness becomes harder to trust.

That creates the final contradiction.

A policy designed partly around harm reduction may increase harm if it drives vulnerable or value-sensitive players towards unlicensed sites.

That is why the UK gambling tax rise could backfire.

Should 40 Percent Remote Gaming Duty Be Reduced?

Global Casino Games’ view is that 40 percent is too high.

The rate should be reduced, or at least reviewed quickly against real market evidence.

A more balanced rate nearer 25 to 30 percent would still represent a meaningful increase from 21 percent. It would still raise revenue. It would still signal that online casino gaming carries harm risk.

It would place less shock pressure on the regulated market.

The government should not wait three or four years to ask whether the policy damaged competition or strengthened the black market.

This kind of market shift can show up sooner. Eighteen months may be enough to reveal changes in bonuses, operator exits, affiliate deals, advertising spend and illegal search activity.

The state should measure the policy against outcomes, not intentions.

If harm falls, channelisation stays strong and tax receipts hold, the case for the rate improves.

If legal market value falls, illegal traffic grows and competition weakens, the case for reduction becomes stronger.

What Would A Smarter UK Gambling Tax Policy Look Like?

A smarter approach would still tax gambling. It would not pretend harm does not exist.

But it would protect the competitiveness of the licensed market.

The state should tax gambling, regulate operators, restrict misleading promotions, punish unlawful firms and fund enforcement properly.

It should also remember why the regulated market exists.

The regulated market is where games can be tested, operators can be fined, complaints can be made and taxes can be collected.

The illegal market offers none of that.

A tax rate that damages the regulated market may look tough. It may not be wise.

The better policy would combine fair taxation with strong channelisation.

That means keeping players inside the regulated system, not pushing them outside it.

Final Editorial View On Why 40 Percent Remote Gaming Duty Should Be Reduced

The UK gambling tax rise sends a clear political message.

Online casino gaming has grown fast, carries harm risk and should pay more.

That argument deserves respect.

But 40 percent Remote Gaming Duty appears too high.

It risks reducing competition, weakening smaller operators, cutting marketing, lowering affiliate revenue, reducing player value and strengthening illegal sites.

The black market does not pay UK tax. It does not follow UK safer gambling rules. It does not need to protect players.

It only needs to look attractive when a player feels tempted.

If the government taxes the licensed market so heavily that activity leaks into illegal gambling, the policy may not reduce harm.

It may move harm into darker corners of the internet.

The UK gambling tax rise may raise money today. The real test is whether it still protects players tomorrow.

This article uses public data and statements from HMRC, the Office for Budget Responsibility, the UK Gambling Commission, the Competition and Markets Authority, the Financial Conduct Authority, IPPR, Reuters, iGaming Business, ICLG, SOFTSWISS, FDJ United, and the Betting and Gaming Council. Source data reflects public information available at the time of writing in June 2026.